Reducing Operating Costs is not Cost Cutting

All too often, cost reduction measures – even where results look impressive at local level – don’t result in the anticipated benefit to the bottom line or, at best, are short–lived. In extreme cases, total cost can even go up rather than down.

Typically, there is a short–term focus on ‘cost cutting’ driven by an imperative requiring urgent cost reduction to meet, for example, quarterly or annual budgetary targets. The result is often a ‘knee jerk’ approach that produces a ‘piecemeal’ response that does little to address the true operating cost of the business and often produces a result that is actually detrimental to the business.

What’s needed for sustainable reductions in operating cost that make a real bottom line difference is a more strategic, ‘whole system’ approach.

The big reductions in Operating Costs don’t

come from Operations!

When talking about Reducing Operating Costs, the big focus is usually in Operations – Production, Warehousing, Supply Chain Management and so on. After all, that’s where the costs are incurred, so it makes sense, right?

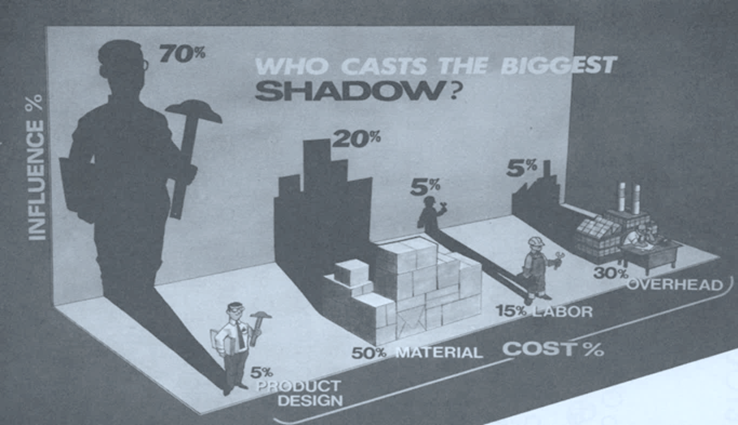

Wrong! If we step back and look at how operating costs are made up, it becomes clear that the vast majority of the cost of Operations is as a result of the consequences of decisions made elsewhere in the organisation. Studies repeatedly show that anything between 70 and 90% of the cost of a product or service are fixed by decisions made before it reaches operations.

This famous image from Munro & Associates shows that, while product design reprsents a small fraction of the cost of a new product, its influence on that cost is huge!

So, while there are undoubtedly savings to be made within Operations itself, a taking a ‘whole system’ view can identify far greater opportunities in the wider organisation.

Click here to learn more and find out how to identify and unlock those opportunities

For such an approach to work, several elements are needed:

A ‘system’ where everyone identifies opportunities and they are recorded for action.

Functions, departments, teams and individuals are open to opportunities identified elsewhere but where they are best placed to take action.

There are mechanisms in place that ‘allow’ actions to be taken that are best for the business as a whole.

What’s it worth?

While such a system may take some time to implement and for the bigger opportunities to filter through to tangible operating cost savings, the potential is huge – up to 10x the savings that are possible through looking at operations alone.

Ready to explore further?

If you’d like to explore these ideas further, the best next step is a free, no obligation call. No sales pitch, just an open conversation to understand you and your business better and see where we can help.

Use the button below to book a call or fill in our contact form and we’ll be in touch.

A better approach to short-term cost reduction

Notwithstanding the general thrust of this topic that a more strategic, ‘whole system’ approach is needed to achieve sustainable and ongoing reductions in operating cost, sometimes short–term tactical action is needed. However, even here, the way you go about it can help or inhibit the longer–term strategic effort, as I discovered many years ago.

There was the usual end–of–year panic. Sales hadn’t hit expectations and we needed to reduce costs to hit year end targets. I’d been to a briefing where one of our directors outlined the challenge and asked us to encourage our teams to avoid unnecessary expenditure. He likened it to “using up what’s in the freezer rather than going to the supermarket”.

I went back to our office and briefed the whole department, explaining the need and asking them to come up with ideas on how we could achieve this. Ideas started to flood in and by the end of the week we had a plan. For example, everyone emptied their desks of whatever stationery items they had hoarded away and committed to making only urgent phone calls in the mornings (this was in the days of landlines and pay–per–call where calls before 1pm were more expensive).

The result: positive engagement led to lots of little actions that made for a significant saving without any detrimental impact on the business.

Shortly afterwards I discovered – during conversation on a coaching course I was running – other managers had taken a different approach. They created “rules” like “don’t buy any stationery” and removed outgoing call privileges from all phones but the one in their office (often locked when they were out at meetings).

The result was very different. Resentment and complaints from staff, workarounds to the rules, empty stationery cupboards and urgent phone calls not made, leading to business disruption and, I can imagine, very little by way of cost saving.

Same objective, different approach, very different result. Which would you use?